Road to Financial Freedom

Finance

Investing

Wealth

Growth

Strategy

Success

Blog posts

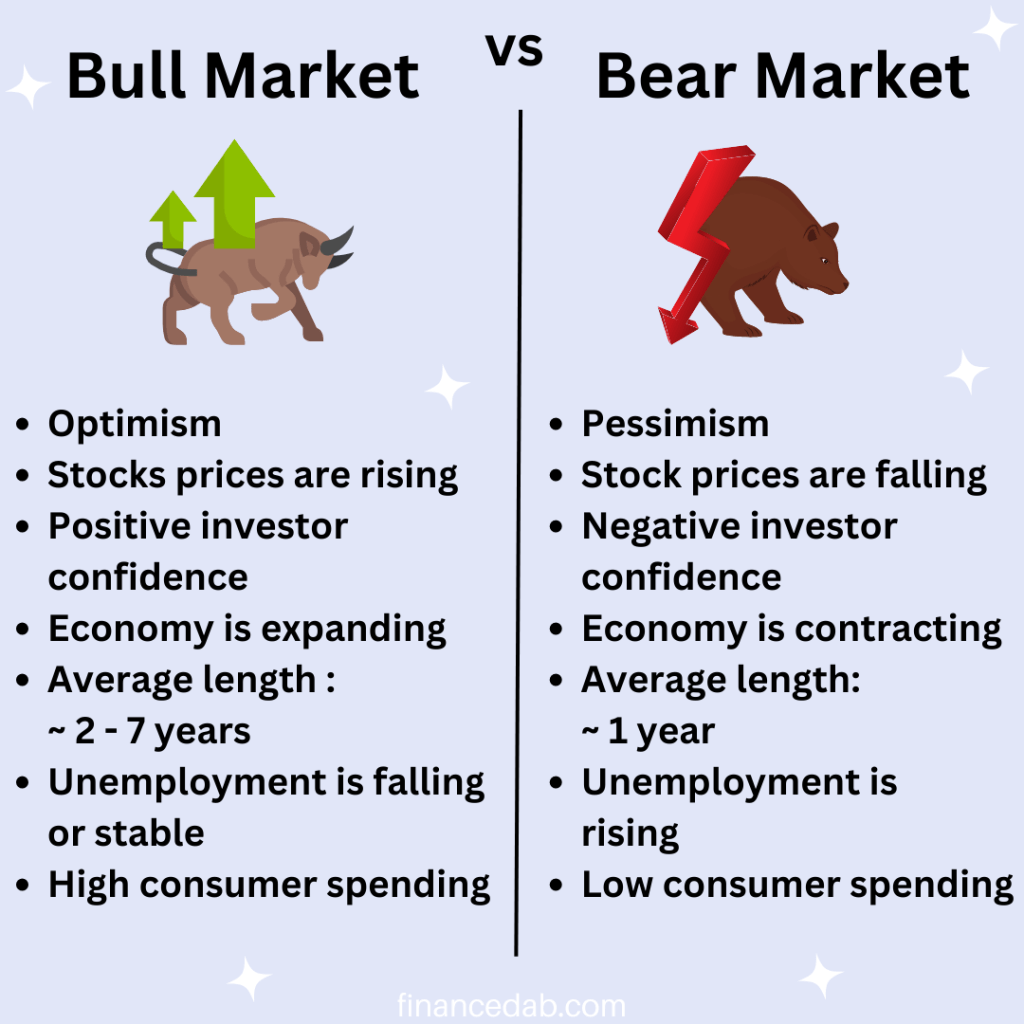

What is the difference between a Bull and Bear market?

February 1st 2023

Bull and Bear market are simply descriptions of how the market is doing.

When you are bullish you are optimistic about the market and when you are bearish you are pessimistic about the market. A bull market means that the market is experiencing a positive trend in pricing while the bear market means the opposite.

When the market index increases by at least 20% from a recent low over a period of at least 2 months, we have a bull market, the investors are optimistic about the future. The economy is strong and unemployment is low or decreasing.

In a bear market, stocks are down by at least 20% or more from recent highs over a period of at least 2 months .

We are currently in a bear market. A bear market is usually caused by a slowing economy and rising unemployment rates. When this happens, the investors feel pessimistic about the market outlook and this can lead to a recession. This situation can create panic when investors try to sell certain investments to protect their money, which creates a sell-off and decreases the prices of the stock market even more (making investors lose even more money).

Bull Market Characteristics:

• Optimism

• Stocks prices are rising

• Positive investor response: high confidence

• Economy is expanding

• Average length : ~ 2 – 7 years

• Unemployment is falling or stable

• High consumer spending

Bear Market Characteristics:

• Pessimism

• Stock prices are falling

• Negative investor response: low confidence

• Economy is contracting

• Average length: ~1 year

• Unemployment is rising

• Low consumer spending

• Could be followed by a recession

During the Bull market, demand is high and supply is weak, we have a high GDP, strong economy, more trading, higher number of international investments, higher liquidity, growing corporate earnings, etc.

While during the bear market we gave low demand with high supply, low GDP, weak economy, less trading, lower number of international investments, lower liquidity, lower corporate earnings, etc.

Investment principles :

- Sell high during the bull market and buy low during the bear market.

- Do not sell off your investments during a bear market when the prices of the stocks are very low – Market timing is extremely difficult, even for professionals.

- Make sure your portfolio is diversified to endure either situation.

- Take advantage of the low prices during a bear market – keep investing – try dollar cost averaging if you are far from retirement.

- If you are near retirement, readjust your portfolio regularly.

- If you are currently retired, the best idea would be to readjust your portfolio to capital preservation instead of growth.

Disclaimer: This article is not meant to be financial advice, please contact your advisor if you require assistance. All articles and data on this page are for informational purposes only.

Tips to Avoid Debt During the Holiday Season

December 1st, 2022

The holiday season is a beautiful time of the year. It is supposed to be a happy period since it is spent with friends and family. But it can often turn into a stressful period if you do not have a plan and a budget in place. We all want to be generous and have successful holiday parties but this can come with a hefty price tag. The last thing you want is to start the new year with a pile of debt to repay. According to US News, 42% of Americans expect to get into debt during the holiday season. On average, a family can easily spend over $700 during the holidays and the amount only increases if you have a big family.

Here are some tips to keep in mind during the holiday season to avoid debt:

1.Create a Plan and shopping budget first – based on what you can afford

The first thing you need to determine is how much money you actually have and how much you can save for the holiday season without getting into debt. This includes both gifts, meals, travel, etc. Check how much money you are spending right now, how much you are saving & investing and how much can be left over for the holiday expenses. Trust me you will be glad you did. If you end up in debt after the holiday season there are chances that you will have to hold off on that well deserved vacation or that car that you have been waiting for. Having a budget will ensure that your expenses are reasonable, and you will be more careful with impulse purchases.

Reminder: Make sure that you calculate all the expenses and not just the gifts!

2. Stick to that budget no matter what –Once you have set a budget make sure that you do not go over it. There are always ways you can decrease expenses by finding other cheaper options. For example; get a chicken for supper instead of steak, or a smaller gift for your cousin. Little extras can add up quickly.

3. Keep track of your expenses

The best way to ensure that you do not go over budget is to keep track of your expenses. This can be done daily or weekly. You can use an app for this or simply a pen&paper, an Excel sheet or anything else you feel comfortable with.

4. Start saving in advance

It is always a good idea to start saving for the holidays as soon as possible. We usually look at our statements around July and then plan for the holiday season. The best advice would be to make a holiday spending account separate from other accounts to make sure that this money is not being used for something else.

5. Make a list of all the people that you need to buy a gift for and check it twice!

Make the list, check the list twice and try to eliminate names on the list. For example, are you able to eliminate the coworkers, the neighbors, some family members, and casual connections? If the answer is yes; then perfect, you can save some money here!

Tip: Make sure you only purchase one gift per person!

6. Set a dollar amount limit per gift – Be frugal

Now that you have a list, put a dollar amount you plan on spending next to each name.

We all like to get into the holiday spirit but it is really important to ensure that the amounts per gift are reasonable. If you are not able to remove people from your list, then try to decrease the amount you have budgeted for each person. Please remember that a gift is just a bonus.

7. Avoid getting gifts for everyone

If you have a big family, make a suggestion to do a gift exchange by picking only one name out of a hat with a specific dollar amount attached to the gift. This will save you a lot of money and stress. Also, you really do not have to give gifts to everyone! Stop feeling bad about not giving a gift to the dog walker, the cousin, the brother in law, etc!

8. Leave a little wiggle room in your budget when you buy gifts to ensure that you do not go over the total amount, in case you need to add someone at the last minute and to make sure you cover the shipping & other expenses.

9. Do a potluck

Instead of spending $500 on a holiday supper/lunch, ask people to bring their favorite dish or drink. This will help your budget a lot. You can keep track of all the items that people are brining to ensure that you have everything you need. Do not feel bad about asking your friends and family to pitch in. Afterall, people are there to spend time with you and not for the supper/lunch itself.

10. Plan gifts in advance

- Planning ahead can give you time to buy things on sale and to find coupons/discounts, etc.

- Planning ahead will give you time to make sure that you are purchasing a meaningful gift

- Planning ahead will give you a peace of mind that the gift will arrive on time if it is purchased online or that the store has the gift you are looking for in stock.

- Planning ahead will give you time to check out the cash saving apps that will give you points or cashbacks!

- Lastly Planning ahead will ensure that you do not overspend because of the last minute stress shopping!

11. Give people the gift of time

Instead of buying a physical gift you can also give people the gift of time.

For example:

- Help them with a project

- Use your skills to help them with something they are not familiar with

- Schedule a volunteering activity

- Schedule a babysitting night for those who have children

- Help individuals with sick family members, etc.

12. Do activities with your family/friends that do not involve money

There are a lot of activities that you can do with family and friends that do not involve money such as:

- Volunteering: at a soup kitchen, at a retirement home, etc.

- Walks

- Board games

- Singing carols

It is about the experiences and not the gifts!

13. Stay away from expensive gifts!

I have seen many individuals buying expensive gifts to prove their love to their families and friends. Please remember that it is the thought that counts and not the amount of money that you spend on gifts.

14. If you are in a bad financial situation; tell your family/friends

When your family is aware that you have financial troubles they will not have any expectations when it comes to gifts or suppers. Be honest if it makes sense for you to skip the gifts this year.

15. Make gift exchanges for kids only or/and give group gifts

Another way to stay within budget is to suggest to your family and friends that the gifts should be only for the kids or plan for group gifts. You can propose Secret Santa – pick a name out of a hat, that way you only have to purchase one gift only. If they agree you can discuss an amount per gift that works for everyone.

16. Do not use your credit cards unless you can pay the amounts in full at the end of the month

Do not forget that credit card interest rates have increased! This means that you are going to pay much more than before if you do not pay off the full amount each month!

17. Take advantage of credit card cashbacks if you can pay the balance in full at the end of the month

As long as you are able to pay the credit card balance in full each month it is a good idea to take advantage of the points that some credit cards offer. A lot of credit cards offer points that can be exchanged for gift cards that you can use during the holiday season.

Other credit cards can provide you with cheaper travel options and insurance.

18. Regift

Regifting has a bad reputation but there is nothing wrong with regifting! If your cousin gave you a frying pan and you already have 2, it is ok to regift that to a friend who just moved into a new house, or someone else who needs one and will appreciate it.

19. Reinvent gift giving

Holiday gifts do not have to be material things. You can make a donation in someone’s name, regift a book, grow plants to give or create gifts. Let your imagination run wild.

20. Or simply: Don’t buy/give gifts

Another option is to tell everyone that you will not be getting gifts and that they should not be getting you gifts either. At the end of the day the holiday season is about spending time with family and friends. It is a time to create memories; build a snowman, watch movies, make cocktails, wear ugly sweaters, play games, etc.

BONUS:

*Beware of impulse spending

Retailers are excellent at enticing people to spend more money! Think about the lighting, the décor, the holiday music to get you in the holiday spirit and spend more money. Don’t get fooled and stay in your budget.

*Try to buy local when possible

When you buy local, you are supporting your communities. Instead of buying something at a big chain such as Walmart, buy something from your local store around the corner. By buying local you are supporting your neighbors and their families. During Covid the owners of the little shops suffered a lot of losses and if you are in a giving mood, it would be a great thing if you could support those little shops.

*Avoid big purchases until after the holiday season such as; appliances, tvs, etc. unless the price is too good to pass up. If you want to make sure that you are able to stay within the allotted budget, try to move leave the big purchases until after the holidays if possible.

*Learn how to make some extra cash for your holiday spending

If these tips are not enough in your case and you absolutely need to spend more than you can currently afford, we recommend you create additional income sources. You can take a side gig before the holiday season in order to cover these expenses instead of taking on debt.

Some interesting ideas can include:

- Online contracts/projects

- Selling your art/hobbies online

- Selling items that you no longer use or need

- Baking/Cooking

- Tutoring

- Getting a part time job on weekends – many organizations are hiring part time employees such as: Purolator, big retail stores, etc.

- Shoveling snow or cutting grass in warmer climates

- Dog walking and pet sitting

- Take surveys online

- House sitting

It is important to remember that inflation has hit most countries at around 8-9% so whatever you purchase this year will cost you 8-9% more than last year. Most salaries have not increased enough to fight inflation, so give that expensive gift a good thought before swiping the credit card without a plan.

The most important thing to remember during the holiday season is that your family and friends care about you and would not want you to get in debt because of gifts. They want to see you happy, healthy and stress free.

10 tips to prepare for a recession

A recession is a significant decline in economic activity that lasts several months. Along with recessions, we see: layoffs, declines in customer spending, stock markets tumbling and an increase in bankruptcies. The media outlets discuss this daily and being surrounded by this negativity can create discomfort and fear.

It is important to understand that recessions are part of the regular business cycle and we have lived through previous recessions and persevered, this time will be no different. Also, experts are predicting a mild recession this time, not the same type of recession we were faced with in 2008.

In order to ease anxiety, it is always good to be prepared. Here are 10 tips to prepare for a recession. But even if there is no recession, you should still follow these tips to achieve financial success.

1. Start with a budget review – update it and tighten it

• If you do not have a budget, it is a good time to create one, take note of all your current monthly expenses such as: food, housing, debt, utilities, etc.

• Your daily spending decisions make a difference.

• Make sure you do not go over the budget that you allocate monthly.

• Delay big purchases for now if you can (for example: cars or houses or renovation projects, etc.).

2. Get rid of unnecessary expenses now – reassess your financial priorities

• Get rid of expenses such as: unused subscription, unneeded clothes, kitchen gadgets, etc.

• Prioritize your spending and what is important – adjust your behaviour accordingly.

• For example:

o skip expensive dinners, go for a drink or dessert instead.

o call the internet provider, your mobile phone carrier, your car insurance company, etc. to see if they can give you a better deal! You will not receive it if you do not try! You have to call to negotiate.

3. Secure 3-6 months’ worth of expenses in your Emergency fund – in a liquid account

• It is important to have some money put aside for emergencies – a financial cushion in case of a job loss or other emergencies – and I understand that this is not always an easy task.

• Start small! Start by cancelling that Doordash order (and saving that money) and making food at home for a fraction of the cost. Or ask your manager for a raise, do a potluck when gathering with friends, etc.

• Save as much money as you can, make it a habit, pay yourself first.

• Set up automated deposits to ensure that you do not forget to set this money aside.

• Having an emergency fund will reduce your stress.

4. Pay off high interest debt

• Make sure to pay off the high interest debt such as credit cards.

• The interest you pay on your credit cards is great income for banks and they love taking that money from you monthly, please don’t give them that pleasure and pay your balances in full each month.

5. Negotiate your high interest debt if you are not able to pay if off

• Speak to your financial institution’s representative to see if you can negotiate your rates if you feel like you are swimming in debt, all you have to do is give them a call.

• They can maybe lower your interest rate, create a repayment plan, consolidate your debt or negotiate other terms.

6. Review your investment portfolio with your financial advisor and keep investing for retirement

• Don’t stop investing for retirement, just pivot your strategy if necessary.

• Diversification is important.

7. Invest in yourself

• Invest in yourself and your future. The world is changing fast and chances are that you need to either polish your current skills or learn new skills.

• Take new courses, read books, etc.

• No job is “recession proof” but if you have marketable skills, it will be harder for your employer to let you go or if you are let go you will not have a hard time finding another job if your skills are in high demand.

8. Create multiple income streams

• The best way to secure an income is to have several streams of it.

• Consider starting a passion project to bring in supplemental income. Invest time in creating a blog, selling items online, getting contracts on the side, etc. You will not regret it.

9. Capitalize on opportunities & stay invested in the market

• “Get greedy when others are fearful” – Warren Buffet

• During recessions stock market prices usually crash so investments are very cheap, it is the perfect time to buy investments with strong balance sheets, strong cash flows and great products/services.

10. Don’t panic & take care of your mental health

• Recessions can be very stressful but as mentioned before they are a part of the business cycle, this too shall pass.

• Be mindful of your mental and emotional stress.

• Whatever you do, do not panic and stress about the recession. The best thing you can do is prepare as much as you can.

• This is not the first time we will be faced with a recession, it is important to stay calm and not do irrational things such as : selling investments at a loss.

Bonus:

Don’t try to time the market

• Even experts cannot accurately time the market.

• It’s impossible to know the best time to get out of the market and when to jump back in at a better time.

If you cannot follow some of these tips because you are simply living paycheck to paycheck and your finances do not allow you to save or to pay off debt, you need to identify opportunities to increase your income if there is no way to cut back on your expenses.

Consider:

• Moving to a less expensive neighborhood if that is possible

• Developing a new skill

• Negotiating a raise

• Finding a better paid job if negotiating a raise does not work

• Creating passive income streams

• Freelancing, contracting, etc.

• Taking an extra shift or working an extra day on weekends

In conclusion, if you follow these tips you will definitely be prepared and less stressed.

Disclaimer: This article is not meant to be financial advice, please contact your advisor if you require assistance. All articles and data on this page are for informational purposes only.

Are we in a recession?

October 27, 2022

A recession has not been officially declared. Even experts don’t know for sure when it will happen or if it will happen at all. But one thing we do know for sure is that; the risk of a recession is high right now. According to JP Morgan Chase CEO, Jamie Dimon, the world economy may enter a recession in 6-9 months.

What is a recession?

A recession is a general slowdown of the economy that lasts more than a few months. A good rule of thumb is: two consecutive quarters of negative gross domestic product (GDP) growth – this means that the economy is shrinking. If we relied solely on this definition, we would say that the U.S. entered a recession in the summer of 2022. But this does not tell the full story, there are other parameters that we need to look at before declaring a recession.

Recession Signs/Indicators

There are many indicators that experts look at when they analyse the economy and the risk of a recession. Some of the main signs of a recession are:

- Decline in real GDP

- Real GDP indicates the total value generated by an economy (goods and services produced) in a certain period.

- Decline in wholesale/retail sales

- A decline in wholesale/retail sales indicates consumer spending decline. When consumer spending decreases, layoffs begin, personal finances and consumer confidence in the market decline.

- Decline in real income

- Real income is calculated by measuring personal income, adjusted for inflation.

- Decline in employment

- The rate of unemployment is a lagging indicator, when we see unemployment rising above 7% it is seen as problematic and could be a sign of a recession.

- Decline in industrial production

- Output that covers manufacturing, mining, electricity, gas, etc.

- Inverted yield curve

- When short-term bonds pay higher yields than long-term bonds, it is called an inverted yield curve. This is typically a sign of an impending recession, as the market believes economic growth will be weak. The yield curve has been inverted since early July.

- Sustained stock market losses

- Rising inflation

Why are experts saying that we are heading into a recession?

Several experts are claiming that a recession will happen in 2023. Experts can only make predictions based on the indicators they observe. Many say that there will be a mild recession to bring down inflation. They are saying that we are heading into a recession because of:

- GDP growth decline

- Rise in Interest rates (which can lead to a rise in auto repossessions and home repossessions)

- Decline in the construction of new homes

- Geopolitical issues

- High inflation

- Inverted yield curve

Why are some experts saying that we will not be in a recession in a few months?

Some experts say that we might not enter into a recession in a few months because the US has low unemployment rate and higher wages. This translates into: more jobs and higher income and more spending from the consumers.

Current situation:

- Labor market is strong

- Consumer spending is strong

- Businesses have strong balance sheets

In conclusion, a mild recession is inevitable at some point. The only thing we can do is to ensure that we are as ready as we can be once the recession is at our doorstep. It is important to remember that recessions are part of the regular business cycle. We have been through previous recessions and we persevered, this time will be no different.

Source: Reuters

Disclaimer: This article is not meant to be financial advice, please contact your advisor if you require financial advice. All articles and data on this page are for informational purposes only.

Should you invest or pay off your debt first?

13 October 2022

The question that comes up very often from new investors is: “Should I pay off my debt before investing any money?” And the answer is: it depends on the type of debt you have, interest rates on debt, the investment returns, your age, and your goals.

Investing only makes sense if you can earn more on your investments than what the debt is costing you in terms of interest. It is important to understand that focusing 100% on paying off all your debt isn’t always the best option. You have to evaluate the debt that you have.

Types of debt:

There are different types of debt such as: credit cards, student loans, personal loans, mortgages, car loans, etc. Debt that has low interest rates includes mortgages, car loans and student loans. Debt that has medium interest rates includes personal loans and debt that usually has very high interest rates includes credit cards. Credit cards are the worst type of debt if you do not pay the balance in full each month.

For example, if you have a $2000 balance on your credit card that is costing you 19% in interest, it is wiser to pay that off first before investing since the stock market will only be able to produce 8-10% on average on your investment. You are actually losing a lot of money by not paying off your credit card bills in full and on time each month. The credit card is a misunderstood tool that is used by the majority of the population. The terms and conditions on these cards are hard to understand. A lot of individuals do not understand that they are paying interest on interest if they do not pay off their balance in full each month. Banks make money on credit card delinquencies, that is why they do not educate their customers about the dangers of credit cards and how they work. If you cannot pay off the balance in full at the end of the month you should not be using that credit card (unless it was used for an emergency). Banks get you hooked by adding points and rewards to their credit cards but don’t be fooled: nothing is free, everything comes at a price.

Always start paying off the debt with the highest interest first!

Should you invest when you have low interest debt? YES! If you have a mortgage or a student loan; you should definitely invest your money while maintaining your required payments.

Rule of thumb:

As a general rule, anything above 7% interest should be paid off as soon as possible.

- Less than 3%: pay off the debt slowly and invest the rest

- Between 3-7%: do both: invest and pay off the debt

- More than 7%: pay it off as soon as possible! – Pay off all credit card debt right away

Also, if you are feeling overwhelmed with debt; talk to your financial advisor about debt consolidation and check if you qualify for a lower rate.

Steps to help you make a decision:

- Step 1: Evaluate your debt

- Step 2: Pay off debt with high interest first – anything above 7%, especially credit card debt

- Step 3: If you are drowning in debt: Consolidate your debt and ask for a lower rate or a different payment plan

After your credit card debt has been paid off:

- Step 4: Check if you have enough money in an emergency fund (if the answer is no then maybe it is a good time to build an emergency fund and pay off the debt at the same time)

- Step 5: If you have an employer matching program; maximize it (you can pay off debt and contribute to the plan at the same time)

- Step 6: Evaluate your retirement plan with an advisor to see if you are on track

- Step 7: Do your research before investing to make sure that your investment aligns with your goals, time horizon and risk tolerance

In conclusion, investing vs debt repayment does not have to be an either-or decision. You can decide that the best option is to do both. One thing you should keep in mind is that: there are always risks when investing so make sure you understand those risks.

Disclaimer: This article is not meant to be financial advice, please contact your advisor if you require financial advice. All articles and data on this page are for informational purposes only.

Why should you care about Inflation?

29 September 2022

What is inflation and why is it important?

Inflation, inflation, inflation; the word in today’s headlines that cannot be ignored. If you picked up the newspaper over the past few months, you surely have noticed that everyone is talking about inflation these days. And for good reason. We read about: households not being able to pay for their utility bills in the United States, retirees around the world worrying about their quality of life and the increase in food bank demand in many cities.

Inflation is a word used to describe the progressive increase in prices of goods and services over a period of time. More specifically, it means a considerable and persistent rise in the general level of prices over a period. Inflation means that the value of your money is decreasing since the prices are rising – you cannot buy as much as you were able to before – this is why you should care about inflation.

When you hear that the inflation is at 8%, it simply means that the average increase in prices is 8%. This means that your cost of living has increased.

There are several ways to track inflation but the most common one is by looking at the Consumer Pricing Index (CPI). If we look at the monthly numbers we see that: prices rose 8.5% in July in the US and 7.6% in Canada compared to the year prior, according to the most recent Consumer Price Index (CPI) report. However, it slowed to 7% in August in Canada and to 8.3% in the United States.

When inflation is expected, it does not cause issues for the market. But when inflation is not expected, it causes a lot of volatility in the economy.

What is the government doing to fight inflation?

The central banks and the governments monitor inflation and target it at 2%. When inflation deviates from the target, the government can adjust its monetary policy to fight inflation. As we saw over the past few months, the interest rates have been increased by the government in order to slow inflation. (Governments can also try to slow inflation with other actions such as: increasing reserve requirements for banks.)

How does the increase in interest rates lower inflation? The idea here is that: inflation is increasing the prices too quickly so the government will raise interest rates and therefore increase your cost of borrowing. The increased cost of borrowing will in turn reduce your demand for loans and therefore your demand for goods and services. Since customers are spending less now, the prices of goods and services eventually decrease.

What causes inflation?

In the short-term, inflation can be a result of an economy in which people have excess cash that they want to spend or are getting accepted for a lot of loans. When this happens, the companies do not have enough supply and cannot keep up with the increased demand that results from this excess money that customers have on hand, therefore the prices rise. What can also happen in this economy is that: organizations know that they can increase their prices of their goods and services without worrying that they will lose their clients – again because demand for their products is high.

Economists break down inflation into two categories: demand pull inflation and cost push inflation

Cost Push inflation:

- When business expenses rise and are then passed on to customers.

- The reasons for the rise in costs include the rise of raw materials, in oil prices, wages increases, disruptions, etc.

Demand Pull inflation:

- When demand for goods and services increases but supply cannot keep up.

- This happens when demand for products increase, and the supply is not able to keep up with that demand

Factors that are thought to have contributed to the inflation we have today:

- Money supply

- Worker shortages

- Rising wages

- Supply chain disruptions

- Gas prices and policy changes

Why should you care about inflation?

You should care about inflation because: when inflation goes up, the value of your income goes down. You are now able to purchase less groceries than before with the same income you are earning. This means that if you have 100$ in your safe at home today and can buy 50 doughnuts with it, that 100$ will not be able to get you 50 donuts in 2 years. So in simple terms; inflation makes your saved money today less valuable in the future. Inflation decreases the purchasing power of an individual. This is why it is important to have a long-term strategy that aligns with your goals – invest your money accordingly.

Who does inflation impact?

Inflation impacts everyone, especially those individuals who are less fortunate and those who are currently retired. Retirees live on a fixed income that often does not keep up with inflation. Many people who are currently working will have their salaries slowly adjust to inflation, but not everyone’s will be adjusted!

This is precisely why it is important to have a diversified portfolio that grows and fights inflation. Put your money to work!

7 things to consider Before you start investing

So you decided that it is time for you to get your finances on the right track and to start investing. This will be one of the best decisions you make. Why you ask? Because investing is a great way to make your money work for you. Investing involves putting your money in financial vehicles in order to earn a financial return. Although a volatile market as we are seeing today might not be an ideal beginning for new investors, there rarely is a bad time to begin investing.

1. Create a budget

A budget is a spending plan based on income and expenses over a period of time. You can use a spreadsheet or any another document to create your budget; it will give you a snapshot of what is coming in and out of your bank account. Your budget will help you determine how much money you have left to invest.

2. Prepare an investment plan

Your money investment should have a purpose. You should have defined investment goals in your plan. Having a purpose will help you determine how you will invest your money. For example, investing to have enough funds in your child’s education fund in 18 years would not be the same as investing to buy a new home in 7 years. You could potentially take on more risk when you have a longer time horizon. Therefore, you should include a timeline and information on how you want to achieve your goals. It does not have to be a fully detailed plan when you get started. We always recommend consulting a financial advisor but if that is not possible; a simple plan is better than no plan at all.

3. Build an Emergency fund

Before you start investing you should have an emergency fund in place. An emergency fund is money put aside that can cover 3 to 9 months of basic living expenses if something unexpected happens to you such as: loss of employment or family illness. By having an emergency fund you will not be stressed out if your investment portfolio value fluctuates and you will not worry about taking on new debt if something goes wrong. (for more information about emergency funds please read our article on emergency funds)

4. Pay off your debt – especially debt with high interest rates such as credit cards

Why is paying off your credit cards extremely important before you start investing? Because the market returns on average 7-10% per year and you are paying 18-20% on your credit card balances! This does not make financial sense because you are paying more than you are able to get from investing. Therefore, you are better off saving as much money as you can and immediately paying off the credit cards. Credit cards are my least favorite tool because a lot of individuals misuse it. They think this is a: “get now, pay later” kind of tool, but in fact it only works in your favor if you are able to pay off the amount owed in full each month when it is due. However, if you have some student loans that are 4%, these should not stop you from investing.

5. Know your risk tolerance

Investments carry risks that need to be considered. Before you start investing you should know how comfortable you are with volatile markets. This will help you determine your investment portfolio. You have to know if you are a conservative investor or not. There are multiple tests online that you can take for free. The most important thing is to be honest with yourself when you take these tests. This will save you a lot of stress and headaches when things do not go according to plan. Will you be able to sleep well at night or will you be awake stressing over your finances and your future if your portfolio decreases in value? Will you have night sweats or sweet dreams? This is an extremely important point to consider.

6. Understand the basics and Stick to the basics – Keep it simple

a. Make sure you understand the basics: stocks, bonds, mutual funds, etc.

b. Do not invest in anything that you do not understand

c. Do not listen to “investment gurus” that you see online – these are usually people who are here to make a quick buck at your expense

d. Always do your own research

e. If you are investing in individual stocks make sure that you understand them and that they will be relevant in the next 10 years. Ask yourself what their financials are and what their competitive advantage is

f. Understand the basic metrics of stock investing

7. Get advice from an expert

A lot of individuals like to get advice from financial advisors. Advisors are great because they can answer your questions quickly and are able to guide you in the right direction . But there are also many other reputable sources that you can use to help you with your investing decisions such as books or articles or online forums. Beginners should always seek help to be able to invest in the long term growth of their portfolio and to be able to allocate their portfolio to get the most value and build strong financial performance. There are many investment options out there and this could be very confusing. In addition, there are many fees that could be charged to your account that you need to understand before making an investment decision.

7 Different Types of Income Streams

Securing different income streams is essential in order to reach financial freedom. It can help you earn extra money and it gives you freedom to not rely only on your salary/hourly work. What would happen to you if your manager decided to let you go tomorrow? Would you be able to survive? Would you have to take on debt? Having several income streams to fall on gives you peace of mind even if it only pays a fraction of your salary for now. Something is better than nothing. The quicker you act the better! There are two types of incomes: active and passive.

Active vs Passive Income Streams

Active income is earned by exchanging your time for money; it consists of your salary. It could be your full-time job, hourly work or even sales commissions.

Passive income is not directly tied to the work you do daily by exchanging your time for money. Beware of the name! This income is earned by investing an amount of time/money upfront and receive income when you are not actively putting additional time/money into it. For example: an online store. The work at the beginning is to build the website, upload your products, and then promote them. The passive income comes later as people begin to buy products from your store. It’s passive, you make money when you sleep. By working on Passive income streams, you will become financially independent, you will gain time, pay off debt with the extra money and in most cases you will be able to work from anywhere around the globe (since most of the set-ups can be managed online).

Types of income:

• Earned Income – Salary

Earned income is your primary source of income: Your Salary. This is how most individuals earn their income and for some it is their only source of income. When you get your salary you are exchanging your time for money. The school system teaches our children that they must have good grades, get a degree and get a job. There is no focus on other income streams which is problematic since the world has changed but our education curriculum has not. A lot of individuals who only have a job live paycheck to paycheck because most salaries do not pay well enough. It is best to diversify your income streams instead of solely relying on your salary.

• Capital Gains Income

When you buy and sell different assets you can receive capital gains when the asset increased in value. Beware of the tax rules that apply to where you live, each region has their own tax rules for capital investments.

• Interest Income

Interest income is generated by investments such as certificates of deposit, savings accounts, peer to peer lending or other vehicles.

• Dividend Income

Dividend income is generated when you purchase shares in companies that pay dividends. This is a passive income strategy from investing in stocks.

• Rental Income

Rental income comes from purchasing real estate and renting it out. It is a great way to invest but does have some disadvantages. The initial investment in real estate property is high, you need to have a down payment, and you need to be able to do repairs to the property if needed. Real estate investing is definitely a long-term investment.

• Profit Income

Profit income is received when you sell a product for more than it cost you. As mentioned by several finance books, the idea is to: Buy low, Sell high. For example, this income could come from opening your company and selling your products or services.

• Royalty Income

This is a passive income stream and it is generated by making or designing or building something original that others pay you to use. In short, others are paying you for using your ideas.

• Other income

The question that I get most often is: how many income streams should I have? And the answer is: As many as you can! But you should pick the income streams that are right for you based on your interests, skill set, risk profile, time, etc. Please keep in mind that the more income streams you decide to try, the more organized you need to become to ensure proper tracking and monitoring of the results. This is why most individuals only pick a few that they are able to manage properly based on their time commitment.

FINANCIAL FREEDOM

Before jumping into the steps to financial freedom it is important to determine what financial freedom means to you. Every person will have their own definition of financial freedom. Our definition here is to be able to do what you want when you want without worrying about money. Don’t confuse this with financial independence which is simply: being able to take care of yourself without relying on someone else. Financial freedom is about taking care of your finances in such a way that you never have to worry about money. It is about making your money work for you. Research from the Thriving Wallet survey (from Thrive Global and Discover) shows that 90% of Americans admit that money has an impact on their stress levels and that money is their number 1 stressor. In order to be financially free, you must have a plan to pay off your debts, build an emergency fund and create several income streams. Nobody has ever been worried about having too much money. The worry only starts when there is either too little of it or when bad planning is involved.

1. Learn the basics of finance and understand your current situation

Learning the basics of finance helps you understand where you are at now and where you want to be. Simple understanding of the basics can go a long way. Unless you are in the field of finance or investment, you do not need to have a detailed understanding of all the terms and their definitions. You only need the basics and that is not very hard to get on top of. Remember: it is never too late to start learning the basics to finance. “Investment in knowledge pays the best interest”- Benjamin Franklin. By understanding basic terms you are already in a better place than most individuals.

You should be able to compile your list of debt (Mortgage, student loans, car loans, credit cards, and any other debt that you have accumulated) and the money you have saved up ( savings accounts, retirement plans, stocks, etc) in order to get started. You should know what a budget is, an emergency fund, capital gains, net worth, credit score, insurance, retirement plan, stock, bond, cryptocurrency, etc.

2. Set realistic goals

What is financial freedom to you? How will you get there? What are your goals? Now that you know where you are at, you need to set realistic goals with timelines and action plan next to those goals to achieve them.

3. Create a budget and stick to it – make a commitment

It is easy to create a budget, what is not easy is to actually follow it. You have to be committed to your goals if you want to achieve financial freedom.

4. Live below your means

This is one of the most important reminders in order to reach financial freedom. A lot of individuals spend their hard-earned money on items such as expensive sports cars – which are liabilities. That money could have been invested in the stock market that would earn you interest. Learn how to live way below your means. You have nobody but yourself to impress in this lifetime.

5. Save and invest

In order to reach financial freedom, you need to start saving and investing that money. You can invest in different vehicles depending on your risk tolerance. You can invest in ETFs, Mutual funds, individual stocks, bonds, real estate, cryptocurrencies, etc. There are many choices to chose from. Once you start investing make sure to diversify your investments. You must be aware that investing could be risky but at the same time it is a beneficial way to grow your wealth. Compound interest is key to financial freedom.

6. Secure several income streams

If you are serious about being financially free: you have to secure several income streams. Your salary is your stable income stream; your active income – you are exchanging your time for money. By relying solely on your salary, the chances of you reaching financial freedom or being wealthy are slim unless you have a very high salary. This is why it is important to work on securing different income streams, particularly passive income which enables you to collect money without putting in your time regularly ( it only requires your time to set it up and for maintenance). Securing several income streams will take some time.

Examples of income streams:

- Equity investments

- Real estate investments

- Owning or investing in a business

- Royalties from intellectual property (books, patents, music, blogs, etc.)

7. Pay off your credit card and other debt

Paying off your debt should probably be first action item on your to do list. It is evident that anyone who wants financial freedom must pay off their debts, especially debts that have high interest such as the credit cards. Think about it, if the stock market can return on average around 8-10% and you are paying 19% on your credit cards, who is a winner? The bank or you?

If you cannot get rid of debt right away you can try to use your low interest debt to pay off the high interest debt or consolidate your debts. Be very mindful of your spending patterns. Before making a purchase always ask yourself: Do I really need this? Can this purchase wait a little longer?

8. Build an emergency fund

You should have at least 3 to 6 months’ worth of basic expenses in your emergency fund but the more you are able to save the better it is.

Examples of emergencies that may arise:

- Medical emergency

- Issues that prevent you from working

- Job loss

- Car issues

- Home repairs that were not planned

- Travel expenses

9. Speak with a financial advisor

Not everyone needs an ongoing relationship with a financial planner or investment advisor. However, it would be a great idea to meet with a financial advisor to ensure that you are on track with your goals, to make sure that you understand all the tax rules and to have all your questions answered. Financial advisors work with different individuals and have seen people from different walks of life so they might be able to provide you with extremely useful advice. If your finances are disorganized and you are not sure where to start you should definitely consult a financial advisor. Find an advisor who understands what’s most important to you and why.

10. Never stop learning – curiosity is key

“Curiosity is the engine of achievement” – Ken Robinson

Be curious about finance! Curiosity is an important attribute. Being curious opens your mind to new ideas, helps you understand how the world works and opens a new world of possibilities. What is an even more important attribute is to put what you have learnt into action. Reading about different topics will not only help you with your finances but can lead you to new business ideas, new income streams, etc.

“It is difficult to understand the universe if you only study one planet” – Miyamoto Musashi

***Bonus: Change your mindset about money

According to Jen Sincero in her book: You are a badass at making money, individuals who do not make a lot of money often have negative feelings towards money. They feel money is “bad” and feel guilty for wanting more money. If you are one of these people, you need a mindset shift. You need to look at money as: a tool to get to where you want to be. If we think money is bad, we will not get any! It is plain and simple. View money in a positive light. Shift your mindset from scarcity to abundance and forget everything negative you have been told about money in your past.

In conclusion, don’t be governed by your finances, take back your control. Financial freedom does not happen overnight, it takes time, planning, hard work and patience. Theodore Roosevelt once said: “Nothing worth having comes easy”, remember this when you feel like things are getting too hard. Those who persevere will reap the benefits.

References:

- Thriving Waller Report https://content.thriveglobal.com/wp-content/uploads/2020/02/Thriving-Wallet-Research-Insights-Report.pdf

- You are a badass at making money – Jen Sincero

10 tips to improve your credit score – Your credit score matters

What is a credit score? It is a score that tells lenders the likelihood of you repaying your loan on time based on your history. Your credit score determines what loans you can get and what interest rates you will pay. Therefore, having a good credit score makes your life easier especially when you need a loan. It also determines the premiums you will pay for things like home insurance and car insurance. Therefore, a good credit score can save you thousands of dollars over the years and lets you get that apartment you want.

- Credit scores are calculated using information in your credit reports

- Credit scores generally range from 300 to 850 (900 in Canada)

What is a good credit score?

Lenders generally see those with credit scores of 670 and above as acceptable or lower-risk. When you have a credit score that is above 670 it means that you are considered reliable, and most banks would be able to give you a loan.

10 tips to improve your credit score

1. Review Your Credit Reports

- Review your reports regularly to ensure that there are no errors.

- There are a few companies that you can use to monitor your credit score and these are:

- Equifax

- TransUnion

- These two : Equifax and TransUnion charge a fee

- Some free credit score companies like Credit Karma and Borrowell do exist – you might have different credit scores on these sites

*** Please keep in mind that this score is just an approximation and some organizations either calculate their own score or use the Beacon score – which can only be seen by organizations (you are able to access the Beacon score in the US but not in Canada). These scores can be similar to one another but will never be the same because of the differences in algorithms used to calculate the scores.

2. Dispute credit report errors

- Errors happen more often than you think; therefore it is important to dispute an error that you see on your credit report.

- Why would there be errors on your report? It could happen due to misspelled names, addresses or other information.

- Once you notify the credit reporting agency of the mistake, they will make the changes and your credit score will improve.

3. Ensure to pay your bills on time

- If you want to increase your credit score, you have to make sure that you pay all your bills on time.

- Creating a tracking system and schedule to keep track of monthly bills can help – it could be electronic or written on paper.

- Setting due-date alerts so you know when a bill is coming up can also help you pay bills on time.

- Automating bill payments from your bank account would be the best way to make sure that no bill gets paid late.

4. Consolidate your accounts if you really need to, this will help in the long run

• There could be a temporary drop in your credit score if you enroll in a debt consolidation program, but as long as you make on-time payments your score quickly improves and you are eliminating the debt that got you in trouble. • Contact your creditor if you cannot make a payment. If you are not able to pay for something you purchased, reach out to your credit card issuer right away to discuss hardship options.

5. Don’t close your old credit card accounts

• The age of your credit history is important. The longer the better. If you do not have a choice and need to close some accounts, try to close the newer credit accounts.

6. Aim for 30% Credit Utilization or Less

- Credit utilization matters to lenders. If lenders see that you have a high credit utilization it means that your money will be tied to repaying these loans off and this creates uncertainty about your ability to repay new loans.

- One of the ways you can keep your credit usage low is to pay your balances in full when due.

- Pay off your credit cards that are maxed out first.

- Ask for a credit limit increase (which we do not recommend if you have bad spending habits)

7. Limit your credit card/loan shopping and the hard inquiries that come with it. Only open new accounts when you need them.

• When you apply for new credit cards often (or any other loan) and shop around, you trigger a hard inquiry on your file and it affects your credit score.

• Hard inquiries can affect your credit score negatively and can happen when you apply for a credit card, car loan, mortgage, etc.

• Looking at your own credit report results in a “soft” inquiry on your credit reports, it will not affect your credit score.

8. Do some research when addressing old debt that is with the collections agency to increase your credit score

• Amounts paid to collections agencies still need to be paid but do your research if you plan to repay accounts with collections agencies since this may potentially affect your credit negatively if your case was already written off for good and you reopen that account. Or, if your collections amount is being transferred to a debt buyer and is in transition you may have issues with having it count in your credit score improvement. Always verify your situation with your lender. A collections amount can remain on your credit reports for up to seven years from the date you first miss a payment to the original lender or creditor. Credit bureaus assign late payments to various categories, the longer the payment is past due, the more it can hurt your credit score. Make sure you do your research.

• A collection account will not be removed from your credit report just because the account has been settled or paid – but it does not hurt to ask to have it removed. Some newer algorithms of credit scores do not take old debt in collections into consideration but some older ones do. Newer credit-scoring models from FICO® ignore zero-balance collection accounts. So paying off a collections account could raise your scores with lenders that use these algorithms. But keep in mind that some lenders still use older scoring models that don’t ignore zero-balance collection accounts.

9. Establish a mix of different loan accounts under your name over time – Credit Mix

• Having a credit mix will help you get a better credit score:

o Credit cards

o Mortgage

o Car loans

o Student loans

o Other

10. Monitor your credit improvements

** It takes at least 3 to 6 months of good credit behavior to see a change in your credit score.

Who uses your credit score?

- Mortgage companies

- Insurance companies

- Home insurance

- Car insurance

- Landlords use your credit score to determine if they should rent their apartment to you or not

- Cellphone companies

- Banks / Credit card companies

What affects the credit score? – Your credit history

- Payment History – Did you make your payments on time? (35%)

o How often, How recently, How late were your payments?

o Did you have payments handed over to a collection agency?

o Do you have foreclosures or did you file for bankruptcy?

o The more recent, frequent, and severely negative items have a bigger impact on your credit score.

- Total debt – Credit usage: How much money did you borrow and how much available credit do you have in your accounts? (30%)

o This is the debt you are already carrying

o Are your credit card cards maxed out?

o How many accounts with balances do you have now?

o How much of your available credit is being used currently?

- Length of credit history (15%)

o The longer your credit history the better

4.The types of accounts that you have & Public records (Credit cards, car payments) (10%)

It is always good to have a mix of different types of accounts:

o Credit cards

o Mortgage

o Car loans

o Student loans

5.Recent requests in your account (10%)

o How often did you apply for new credit?

It is important to understand that the credit score varies from person to person. For example, some individuals do not have a long credit history so their score will be calculated differently from a person who has a long history.

Some good news for those who do not have a great credit score

Lenders do look at other information about you and not only your credit score, they will look at things such as:

- Your income

- The type of credit you are requesting

- The stability of your job (how long you worked there, etc.)

- **If you go to a dealership to get a car: they will use their own score.

- **If you want to rent an apartment: they look at the Beacon score.

- **Financial institutions use the Five Cs of Credit to determine the “credit worthiness” of a business owner (meaning, the ability to borrow and then repay money). These five Cs are: Character/ Capacity/ Capital/ Collateral/ Conditions

In conclusion, as long as you pay your bills on time, have a good credit mix and monitor your credit history; your score should be good enough for you to be able to get the loan you need or rent the apartment you desire.

How much should I save for retirement? How much will I need?

Are you worried about not having enough money once you retire? Trust me you are not alone!

There are many discussions around Retirement and experts have different opinions when it comes to how much one should save for retirement. The reason for this is simple: each retirement plan will have a different number assigned to it depending on your goals, who you are, your salary, your expenses and what you want your retirement to look like. Some individuals will cut their expenses by 30% during their retirement while others will travel the world and will need extra funds for their new lifestyle. For example, my aunt decided to sell her big house and move into a small condominium when she retired – this saved her over 40% on expenses such as mortgage, utilities and maintenance. Therefore, the short answer to the retirement question “How much should I save” is: It depends on you and your expectations of the future!

We do however have a good rule of thumb that can be used to make sure you have enough money saved for retirement. The rule of thumb is to save at least 10 to 15% (preferably 15%) of your pre-tax yearly salary for your retirement every year. The more you save the better. Pay yourself first, trust me you will not regret it. This number applies if you start to save early in your career and invest your money; the number increases if you wait longer. Many employers will match your contributions towards your retirement; make sure you take advantage of this!

How much should I have saved at 30, 40, 50, 60 and 67?

The right retirement amount saved will depend on when you want to retire and when you started investing.

Let’s look at the guidelines for a classic case of retirement at 67.

As you can see in the table below the recommendation is to have 1.5x of salary saved for retirement by the time you are 30. But how in the world would you be able to do that? If you examine this number closely you will notice that the 1.5x is simply saving 10-15% of your salary yearly for your retirement from 22 to 30, as most experts will tell you.

| Age | Recommended annual salary saved for retirement |

| 30 | 1 – 1.5 times |

| 40 | 2.5 – 3.5x |

| 50 | 5.5 – 6.5x |

| 60 | 7 – 8x |

| 67 | 9 – 10x |

* Remember: This table is only a recommended amount of salary that you should have saved based on your age and based on the fact that you will invest that money and let the power of compounding do the work. Speaking to a financial advisor would be the best idea to determine if these numbers apply to you based on your goals.

I do not have that much saved, what do I do?

- Do not panic and make a plan.

The most important thing to do is to ensure that you have set goals for yourself with a realistic plan that you will be able to follow. Most individuals do not have the recommended amount of money saved in their retirement accounts, so they have some catching up to do. The plan will involve cutting down on some unnecessary expenses, building different income streams to make up for the difference, etc. - The best day to start saving is TODAY!

Start saving as soon as you can, do not wait for a better time, every penny counts. - Automate your deposits to your retirement account monthly if possible

- This process will ensure that you do not forget or spend your funds on other items. You can adjust the frequency of the deposits.

- Verify if your employer matches your contributions to your retirement account

If your employer matches your contributions try to maximize this opportunity (it is free money!) - Negotiate your salary – we tend to undersell ourselves at work. Ask your boss for an increase in salary – if you do not ask you will not receive! Many individuals wait for their boss to give them a raise or accept no for an answer. If after several attempts of asking for a raise your boss turns you down it might be time to start looking for another job that will appreciate your skills and efforts.

- Assess your spending patterns

Sometimes the reason you were not able to save for retirement is “overspending” on items that you might not need. Learn to live way below your means. - Look into different income streams that might work for you (real estate, stocks, etc.)

- Don’t get distracted – Be disciplined – remember your retirement savings goals when you make decisions.

There are certain decisions that we make in life that will cost us a lot of money. Yes, your wedding is extremely important, but it is not wise to spend money on a wedding at the expense of your own retirement. Check if you can perhaps postpone for a year or maybe have a smaller wedding. What about that expensive car? Do you really need it right now? Can your purchase wait a year or two? - Invest your money! Use the government recognized vehicles such as RRSPs in Canada or IRAs in the US (or others in your home country) since these give you a tax advantage. If you are only saving your money in a checking bank account, it’s going to be very difficult for you to hit your retirement goals – you need the power of compounding – please keep in mind that banks have a very low interest rate that does not even keep up with inflation. The best thing would be to invest in ETFs, Mutual funds, Bonds, stocks, etc.

- Plan to work past 67 if possible. If you are fit and plan to work past 67 then it is ok if you are a little behind schedule since you have time to make up for the funds that are missing in your retirement savings account.

- Don’t forget to consider inflation!

Remember that the dollar you have in your hand today will not be able to buy you the same thing in 20 years but less. - Speak to your financial advisor and review your plan with him/her regularly.

A financial advisor would be the best person to help you with any concerns/questions you may have. They will be able to give you advice that you might not have thought of on your own. They have experience working with individuals from different walks of life and they will be able to determine the best course of action tailored to your situation and needs.

The 4% Rule

The question I get asked most often is: is there an easier way to figure out how much money I will actually need to cover my expenses? And my answer is: yes there is an approximation you can use and it is called: The 4% rule.

So what is the 4% rule?

It is the expenses you will have during retirement divided by 4%. This rule tells you that you can safely withdraw 4 percent a year from your retirement savings portfolio without running out of funds. For example: 30 000$ in expenses / 4% = 750 000$. If you have 750 000$ in your account you can safely withdraw your yearly expenses of 30 000$ without worrying.

Planning for retirement – Questions to ask yourself

It is important to remember that your retirement will look very different from your parents’ retirement. Most of our parents had great pension plans in the past and they were able to retire at 55. This is no longer the case, as many companies no longer offer these types of pension plans (called defined benefit pension plans). In addition, the life expectancy for men and women has increased over the years with new medical developments, which means that you need to make your retirement amount last for several decades.

Here are some questions to ask yourself to help you determine exactly how much money you will need for retirement.

- What are your goals?

- When do you want to retire? At 67 or earlier? The age you plan to retire can have a big impact on the amount you need to save. Delaying retirement gives your savings a longer time to grow.

- How long do you expect your retirement to last?

- Where and how would you like to live during your retirement?

- What income sources will you have post-retirement? Will you work part-time

- Social Security payments from the government (when can you claim it?)

- Real estate

- Stocks, ETFs, other

- Help from children or cousins or anyone else

- What will your expenses be? Will they increase or decrease?

- Will you be selling your home and moving to Thailand?

- Will you be moving into a smaller home? Or a condominium perhaps?

- Will your house be paid off at retirement or will you still be renting at retirement?

- Do you have any expensive hobbies you are planning for?

- Is there any debt you need to pay off before retiring?

- Do you have an Estate plan? Do you have a will? Are you planning to leave anything to your children, neighbors or cousins?

- Do you have insurance? If not it might be worth looking into

- Do you have an emergency fund? Yes the emergency fund is still important during and preretirement to make sure you do not dip into those funds prematurely.

In order to be on track to retire by the age of 65-67 there are several things that you need to take into consideration. The best advice anyone can give you is: Start saving early! The reason why you should start saving early is because of power of compounding, which will make your money grow faster!

Emergency Fund – Rainy day fund

Managing a budget can be very stressful, especially when we have unexpected expenses that creep up on us. So, what exactly is an emergency fund that everyone keeps talking about? In short, an emergency fund is money put aside that can cover 3 to 6 months of basic living expenses if something unexpected happens to you. Emergency funds are extremely important in any strong personal financial plan. As you know, life can throw us unexpected curveballs, which could create a lot of anxiety. By having this money aside, you will have a peace of mind.

Examples of emergencies that can arise:

- Medical emergency

- Issues that prevent you from working

- Job loss

- Car issues

- Home repairs that were not planned

- Travel expenses

How much should I save?

It really depends on your monthly expenses. You should have at least 3 to 6 months’ worth of basic expenses in your emergency fund but the more you are able to save the better it is. Therefore, the first thing you need to do is to estimate your monthly expenses such as:

- Rent/Mortgage

- Groceries

- Insurance

- Car

- Utilities

- Debt

- Personal expenses

- Other expenses

Many individuals do not include nonessentials in their calculations such as:

- Vacations

- Entertainment

- Eating out

- Any other nonessential

These are often excluded because you can survive without these but you definitely have to pay your rent on time and you need to buy groceries as well.

Cannot save that much?

For some individuals it is simply impossible to save 6 months worth of expenses. Fear not, anything you save is better than nothing! Start by saving a realistic amount, it takes individuals months or even years to reach their planed amount of emergency savings. That is normal. You can start small and start excluding certain nonessential expenses from your monthly budget slowly. You can also think about getting another source of income as well! (Discussed in another article) Every penny counts! Start by saving 10$ a week and increase that amount with time if you are able to.

For example:

- Saving $10 a week will secure $520 in a year in your emergency savings account plus any accrued interest

- Saving $50 w week will secure $2600 in a year in your emergency savings account plus any accrued interest

How do I make those savings?

- Be disciplined – monitor your daily habits

- Create savings reminders in your calendar to keep yourself on track

- Be able to determine opportunities to eliminate certain expenses

- Stop and think: Do I really need this new pair of shoes? Can I make coffee at home? Can I purchase this next month? Do I have a coupon to lower my grocery bill?

- Automate your deposits to your emergency fund

- You can pick the frequency and date to make transfers from your checking account to your savings account when you receive your paycheque. This process will ensure that you do not forget or spend your funds on other items.

- Add money to your emergency fund whenever an opportunity presents itself.

- For instance if you receive: a raise, gift, an inheritance or bonus place it in your emergency fund instead of spending it (but first make sure your credit card debt is paid in full before saving that amount because chances are that you are paying a high interest on that credit card).

- Review your financial goals on a regular basis

- Changes happen on a daily basis and you need to ensure that your financial goals are still accurate and that you are on track. If you are not on track, you need to make review your goals, actions, habits, etc

- To help you determine if you need a revision here are some examples of changes in your life that might trigger a review of your financial plan:

- A purchase of new house

- A new spouse

- A baby

- An increase in bills such as utilities or taxes

- An illness in the family

- Other

Advantages of an emergency fund

There are several advantages for having an emergency fund.

- You will have a peace of mind with the emergency fund, less stress about your finances and your future.

- You can handle emergencies without getting into debt and stressing about how you will pay it off later.

- It gives you financial control – because the emergency fund will be in a separate account from your day-to-day transaction account, it will decrease your chances of spending it on things that you do not actually need.

Ok, I have my emergency fund money saved, where do I keep this money?

No, you do not keep this money under the mattress like grandma has taught you.

Your emergency fund should:

- Be easy to access. This will make it easier to take care of an emergency rapidly. It is important to make sure that the account you chose will let you make withdrawals without penalties.

- Be separate from your day-to-day transactions account

- Be in an account that earns you interest. It would not make sense for your emergency fund to sit idle for a few years without earning any interest at all.

- Be in an account with low market risk. You want to know that your money will be there when you need it most – especially during an economic downturn.

In conclusion, saving for an emergency fund is not a fun endeavour but you will be so glad you did it! Hopefully you will not need to use those funds any time soon but if you do at least you will have one less stressful event to think about.

Before using the funds please make sure that the emergency is really an emergency and not a “want” in disguise! For example: your car breaks down and you decide to purchase a brand new awesome one instead of getting your old car fixed.. Was that a real emergency? I don’t think so.

And most importantly, when you use the money in your emergency fund, make sure that you create a plan to replace that money in the future for other emergencies. It is a continuous process: Save money for the emergency fund, Use the funds in the emergency fund, Replenish the funds in the emergency fund.

Budgeting

What is a budget? Why is it important?

A budget is a spending plan based on income and expenses over a period of time. You can use a spreadsheet or another document to create a budget; it will give you a snapshot of what is coming in and out of your bank account. In 2019, the BDO survey found that over 50% of Canadians live paycheque to paycheque and in 2020 Highland found that 63% of Americans are living paycheque to paycheque. This happens because of a lack of income, lack of budgeting and planning, impulse spending and trying to keep up with the neighbours’ lifestyles. By having a budget/plan and sticking to it, you will be set up for success and will not stress about money when an emergency arises. By being aware of your spending patterns, you are able to make changes to ensure that you reach your goals, ensure that you pay the bills on time, etc. With the right tools on hand, this does not have to be a tedious task.

How to build a budget?

It is best to build a monthly budget. Set yourself up today and plan for the future! Building a budget will help you ensure that you are not overspending on things that you do not need and that you are on track to reaching your future goals. This will enable you to shift your mindset and ensure financial security, which will in turn lower your stress levels about your finances. You will not have to worry if you have enough for a rainy day because you will be well prepared for whatever life throws at you.

There are many budgeting tools and templates that you can use. The idea is to track your spending patterns.

1. Google sheets

2. Mint

3. Honeydue

4. Any other budgeting tool, even a pen and paper will do!

Steps to building a budget:

1. Find your recent paystubs, bank statements, credit card statements – you want to make sure that the estimates you make are reliable and accurate

2. Calculate your Net Income: The first line in your budgeting should be your income

3. Calculate your monthly expenses:

a) Figure out what your Fixed monthly payments are – estimates are ok but it is best to build a buffer

b) Figure out what your Variable payments are

4. Now you need to see if you have a surplus (your income minus expenses is positive) or a deficit (your income minus expenses is negative). When you have a deficit in your account, it is not sustainable and changes in your consumption patterns need to be made.

5. Determine what to do with your Savings: Pay yourself first! Before deciding what to do with the remainder of your income after accounting for expenses ensure that you put some money away for your future goals and to your emergency fund for a rainy day! (You can have an amount directly debited from your account and deposited to a different account that you can invest at a later date – this of course should be set-up after you make a proper budget)

6. Make it a habit to track your expenses (it is best to do it right after your payment – this is why the budgeting apps mentioned in this article are so useful)

7. Separate your needs from wants

8. Create goals to cut spending and goals to save/invest

9. Adjust your budget as needed with time and experience

What should you include in your budget?

1. Income – After tax income

2. Monthly/yearly fixed expenses

- Rent

- Utilities

- Phone bills

- Insurance

- Car payments

3. Monthly/yearly variable expenses. These change month to month

- Buying clothes, eating out

- Entertainment

- Grocery bills

***Examples of monthly payments – most people like to categorize their spending: